India Smartphone Market Slows in Q1 2026: Price Rise, Entry-Level Collapse and What It Means for Mobile Shops

India’s smartphone market entered 2026 with a clear warning sign: fewer phones shipped, higher average prices, weaker budget demand and stronger offline retail. This report explains the Q1 2026 slowdown, brand-wise movement, price segment shift, Rajasthan market impact, mobile shop view, old-stock movement and social media discussion around rising phone prices.

India’s smartphone market slowed in Q1 2026, but the story is not just about lower shipments. The bigger change is that the market is becoming more expensive, entry-level phones are shrinking fast, and buyers are being pushed toward higher price bands even when their budget has not increased.

According to IDC’s Q1 2026 smartphone tracker, India shipped around 31 million smartphones during January-March 2026, down 4.1% year-on-year. At the same time, the average selling price touched a record US$302, while market value still grew despite lower shipment volume.

This means India is not simply buying fewer phones. India is buying fewer cheap phones, while more value is moving toward mid-range, premium mid-range and premium devices. For customers, this means fewer good options under ₹8,000 to ₹10,000. For brands, it means pressure to manage memory cost, inventory and pricing. For mobile shops, it means the selling conversation has changed from “lowest price” to “best value with EMI, exchange, service confidence and long-term usability.”

India Smartphone Market Q1 2026: Key Numbers

The clearest message from the numbers is that India’s smartphone market is not collapsing equally across all segments. The pressure is concentrated at the budget end. Phones below US$100 suffered the biggest drop, while the US$100-200 segment grew as buyers moved upward because very low-cost options became weaker or less available.

Why Did the Market Slow Down?

The biggest reason is rising memory cost. DRAM and NAND prices have increased globally because AI data centers are consuming a large share of memory supply. Smartphone brands now have less room to sell very cheap phones with healthy margins.

This directly hurts India because the country has always been a highly price-sensitive smartphone market. When memory cost rises, entry-level phones become difficult to build and difficult to discount. Brands either increase prices, reduce specifications, reduce launches or push customers into higher price bands.

The second reason is weak post-festive demand. Q1 is already a slower quarter after India’s festive season. In 2026, this normal slowdown became sharper because buyers also faced higher phone prices, inflation pressure and fewer aggressive online discounts.

The third reason is longer upgrade cycles. Many customers are now keeping phones for longer. If a customer bought a 5G phone in 2023 or 2024, they may not upgrade immediately unless the battery, display or performance becomes a real problem.

Price Segment Shift: Budget Phones Took the Biggest Hit

| Price Segment | Q1 2026 Movement | Share Change | What It Means for India |

|---|---|---|---|

| Entry-level Below US$100 |

Down 59% YoY | 18% to 8% | The cheapest smartphone category collapsed as cost pressure made low-margin models difficult to sustain. |

| Mass Budget US$100-200 |

Up 10% YoY | 39% to 45% | Many buyers moved into this band because cheaper choices became weaker or disappeared. |

| Entry Premium US$200-400 |

Down 3% YoY | 26% to 27% | This segment stayed relatively stable, helped by 5G, better cameras and EMI demand. |

| Mid Premium US$400-600 |

Up 29% YoY | 6% to 8% | Premium mid-range phones gained from stronger camera, battery and brand-led launches. |

| Premium US$600-800 |

Up 32% YoY | 4% to 6% | Premium buyers remained active, especially with financing and exchange offers. |

| Super Premium US$800+ |

Down 1% YoY | Around 7% | Ultra-premium stayed resilient, led by strong Apple and Samsung demand. |

Graph: Where India’s Smartphone Buyers Moved in Q1 2026

This graph shows the real shift. The US$100-200 band is now the heart of India’s smartphone market. In rupee terms, this is the broad ₹8,500 to ₹17,000 zone before taxes, offers and local pricing. This is where buyers are moving when sub-₹8,000 phones do not offer enough value.

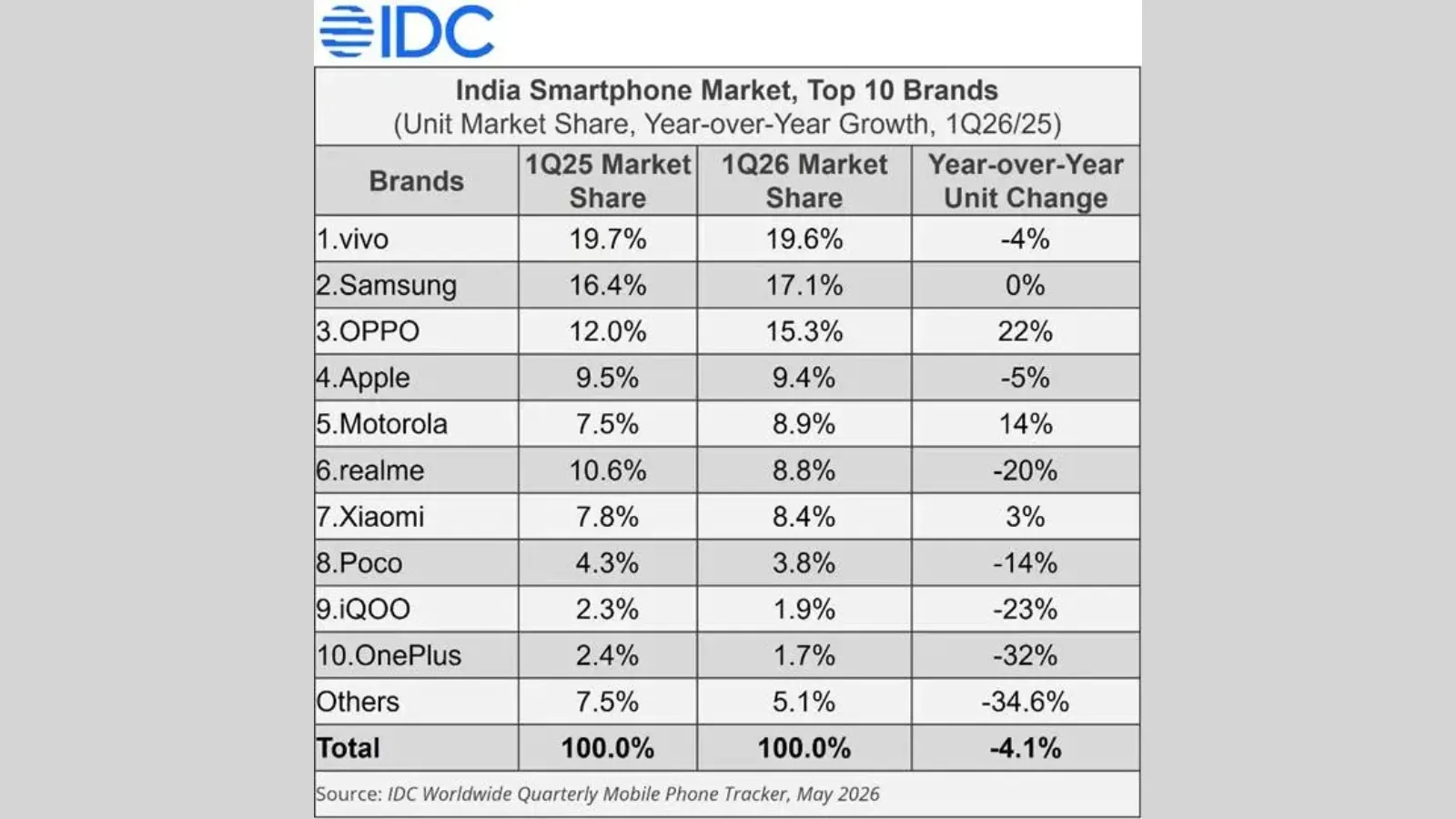

Brand Performance: Vivo Leads, OPPO and Motorola Gain

The Q1 2026 brand table shows a clear split. Some brands gained because they had better mid-range execution and stronger offline presence. Others declined because budget pressure, online weakness or portfolio changes hit them harder.

| Brand | Q1 2025 Share | Q1 2026 Share | YoY Unit Change | Market Reading |

|---|---|---|---|---|

| vivo | 19.7% | 19.6% | -4% | Still No. 1, helped by offline reach and strong mid-range visibility. |

| Samsung | 16.4% | 17.1% | 0% | Stable at No. 2, supported by A-series and premium interest. |

| OPPO | 12.0% | 15.3% | +22% | Biggest top-tier gainer, helped by offline execution and A/K/Reno portfolio strength. |

| Apple | 9.5% | 9.4% | -5% | Volume share steady, but value share remains very strong in premium segment. |

| Motorola | 7.5% | 8.9% | +14% | New top-five momentum, helped by affordable and mid-range phones. |

| realme | 10.6% | 8.8% | -20% | Under pressure as budget buyers became more price-sensitive and portfolio shifted. |

| Xiaomi | 7.8% | 8.4% | +3% | Slight gain, but competition in the budget and mid-range zone remains intense. |

| Others | 7.5% | 5.1% | -34.6% | Smaller brands and low-margin players faced heavier pressure. |

Graph: Top Brand Share in Q1 2026

Why OPPO and Motorola Gained When the Market Fell

OPPO and Motorola stand out because both gained in a market that declined. OPPO’s growth shows the importance of offline execution, consistent store visibility and a balanced portfolio across A-series, K-series and Reno models.

Motorola’s rise is also important because the brand has been building value in the mid-range and affordable premium space. Clean software, competitive pricing and improved retail presence helped Motorola become more visible to buyers who want an alternative to the usual vivo, Samsung, OPPO, Redmi and realme options.

This is a clear signal for 2026: brands that depend only on flash sales or low-cost phones may face pressure. Brands that combine offline visibility, financing, better battery, better camera and stronger after-sales confidence may perform better.

Offline Retail Becomes Stronger as Online Slows

One of the most important points for Indian mobile shops is channel movement. IDC data shows offline retail strengthened to 62% share, while online fell as promotions became weaker and pricing pressure increased.

This is a big development for mobile retailers. In the last few years, many buyers compared online prices first. But when discounts reduce and prices rise, customers again walk into shops to check exchange value, EMI, warranty, touch-and-feel experience and immediate availability.

For small and medium mobile shops, this creates both opportunity and pressure. The opportunity is that offline buyers are coming back for guidance. The pressure is that shop owners must explain price rise, manage customer expectations and keep the right stock mix.

Mobile Shop View: In the current situation, the best-selling conversation in shops is no longer only “which phone is cheapest?” It is becoming “which phone gives better battery, storage, service, EMI and resale value for the price?”

Rajasthan Market View: Jaipur, Jodhpur, Kota, Ajmer and Udaipur

For Rajasthan, this market shift is very practical. Buyers in Jaipur, Jodhpur, Kota, Ajmer, Udaipur, Bikaner, Alwar, Sikar and Bhilwara are highly value-conscious, but they are also upgrading toward better 5G phones, bigger batteries and higher storage variants.

The sub-₹10,000 category becoming weaker will affect first-time smartphone buyers, students, rural buyers and customers replacing older 4G phones. Many of these customers may now stretch toward ₹10,000 to ₹15,000 phones because the lowest-priced options may not feel future-ready.

In Jaipur and Kota, student buyers may still look for performance and battery in the ₹12,000 to ₹20,000 range. In Jodhpur, Udaipur and Ajmer, offline shop trust and brand service network may matter more. In smaller towns, availability, exchange and EMI will decide conversion.

Mobile Shop Ground Reality: Customers May Delay Buying, While Older Stock Starts Moving

Retailer insight: The current slowdown may not be only a demand problem. It may also be a stock-mix problem, where old inventory is clearing but fresh new-launch stock is moving slowly because of higher price gaps.

For mobile shops in Rajasthan, the current price increase has created a different kind of customer behaviour. Many customers are not immediately accepting the new higher prices. Instead, they are postponing purchases with the belief that smartphone prices may come back to normal in the coming months.

This is especially visible in the ₹10,000 to ₹25,000 price range, where even a ₹2,000 difference can change the buyer’s final decision. When a customer hears that a phone which was earlier available at one price has now become costlier, the first reaction is often: “Let us wait, maybe the price will come down again.”

But there is another important shop-level effect. Older models that are near end-of-life, meaning phones launched six months to one year ago and still available in company or channel stock, may suddenly look more attractive than fresh new-launch models.

Earlier, the difference between an older near-EOL model and a new launch SKU was often around ₹2,000. After the price increase, this gap can become much wider — around ₹4,000 to ₹6,000 in some cases. That bigger gap can push customers toward older phones that are already lying in the market.

This means old stock may start moving out, but fresh stock and new imports may slow down. From the outside, the market may look weak because new shipments are down. But inside the retail market, some sales may still be happening through older inventory that was already stuck in the channel.

Old Stock vs New Launch: Why the Price Gap Matters

| Market Situation | Before Price Increase | After Price Increase | Impact on Customer Buying |

|---|---|---|---|

| Near-EOL model vs new launch SKU | Approx. ₹2,000 price difference | Gap may widen to ₹4,000-₹6,000 | Customer may choose older model instead of fresh new launch. |

| Customer mindset | Buyer compared features, offers and brand value | Buyer waits, expecting prices to become normal again | Purchase decision gets postponed or shifted to older stock. |

| Retail stock movement | Fresh launches moved faster with normal price gap | Older stuck stock becomes more attractive | Old inventory clears, but new stock movement slows. |

| Fresh import and shipment impact | Brands pushed fresh imports and new models | Fresh stock ordering becomes cautious | Market trackers may show shipment dip even if some retail sales continue through old stock. |

Graph: Price Gap Between Older Models and New Launches May Widen

This shop-level price gap is important because it can explain why fresh stock movement may look weak. A customer who planned to buy a newly launched model may instead choose an older phone if the difference becomes ₹4,000 to ₹6,000. That helps clear old stock, but it can also reduce demand for fresh launches.

What Indian Mobile Shops Should Do Now

| Shop Challenge | What Is Changing | Smart Retail Response |

|---|---|---|

| Budget buyer confusion | Customers expect old prices, but brands are increasing prices. | Explain memory cost, better storage options and why slightly higher budget may give longer life. |

| Entry-level stock risk | Sub-₹10,000 phones have lower margin and fewer strong options. | Keep limited but reliable stock; push practical ₹10,000-₹15,000 alternatives. |

| Old stock vs new launch | Near-EOL phones may look better because new launch prices have increased. | Use old stock carefully as a value option, but clearly explain launch date, update support and warranty. |

| Fresh stock movement | Customers may avoid new SKUs if price gap feels too high. | Focus on EMI, exchange, launch offers and feature difference to justify new model pricing. |

| Online price comparison | Online discounts are weaker than before in many cases. | Highlight same-day delivery, exchange, setup help, warranty support and trust. |

| Premium buyer expectations | Premium buyers compare camera, battery, AI features and resale value. | Use demo units, camera samples and EMI explanation to improve conversion. |

| Longer upgrade cycle | People are keeping phones longer. | Promote exchange offers, battery-health checks and repair-vs-upgrade comparison. |

Buyer Impact: Should Customers Buy Now or Wait?

For buyers, the Q1 2026 data gives one important signal: the cheapest phones may not become better immediately. If memory costs remain high, budget phones may either become more expensive or compromise on RAM, storage, display or camera.

If a customer needs a phone urgently, waiting only for a big price drop may not work in the short term. Instead, buyers should compare total value: RAM, storage, battery, service center access, software support, exchange offer and EMI cost.

For customers with a phone that is still working well, waiting until festive sales may make sense. But for customers using an old 4G phone, damaged display or weak battery, upgrading earlier to a strong 5G model in the ₹12,000 to ₹20,000 range may be more practical.

Customers should also understand the difference between a near-EOL older model and a fresh new launch. Older phones can be good value if the price is right, but buyers should check software update promise, service support, battery age, storage variant and whether the model still makes sense for the next two to three years.

Social Media Discussion: X, Reddit, Facebook, YouTube and Instagram

The discussion across social platforms is mostly practical, not emotional brand wars. On X, tech accounts are sharing the IDC table and highlighting three key points: vivo remains No. 1, OPPO and Motorola gained, and the overall market declined.

On Reddit-style smartphone communities, users are discussing why entry-level phones are disappearing and why memory cost makes cheap smartphones difficult. Many comments around the market reflect the same concern: if RAM and storage become expensive, the under-₹10,000 smartphone category cannot remain as strong as before.

On Facebook and Instagram tech pages, the discussion is simpler: phones are getting expensive, budget buyers are delaying upgrades and premium phones are still selling. This matches what many shops are seeing on the ground.

On YouTube Shorts and Instagram Reels, the story is likely to be explained through simple hooks: “India phone market down,” “cheap phones becoming expensive,” “OPPO and Motorola rising,” “offline shops gaining again,” and “old stock becoming attractive.” These are easy points for short-form creators because the data affects normal buyers directly.

Business View: This Is a Structural Reset, Not Just a Slow Quarter

The Q1 2026 slowdown should not be seen only as a seasonal dip. It looks more like a structural reset. The market is moving away from ultra-low-cost volume and toward higher-value devices.

This does not mean every Indian buyer suddenly wants expensive phones. In many cases, buyers are being pushed upward because the cheapest segment has become less viable. That is a very different type of premiumization.

There is also a retail inventory angle. Fresh shipment decline does not always mean customers are buying nothing. In some markets, customers may be choosing older near-EOL models because the price gap between old stock and fresh new launches has increased sharply. This can clear older inventory from the channel while fresh imports and new launch stock move more slowly.

For brands, the message is clear. They must manage memory cost, pricing, channel inventory and financing more carefully. For retailers, the message is equally clear. They must sell trust, guidance and value, not only price.

What to Watch in the Next Two Quarters

- Memory prices: If DRAM and NAND costs stay high, budget phones may remain under pressure.

- Festive offers: Diwali season will show whether brands can bring back aggressive promotions.

- Offline retail: If offline share stays above 60%, mobile shops will gain more importance in buyer decisions.

- Old inventory: Near-EOL models may continue moving if the price gap against fresh launches remains high.

- Fresh imports: Brands may stay cautious if new stock movement remains slow in retail.

- Motorola and OPPO: Both brands need to prove that Q1 growth was not only temporary.

- realme, Poco, iQOO and OnePlus: These brands need stronger value messaging to recover lost momentum.

- Sub-₹10,000 phones: This category will decide how deeply the slowdown affects first-time and rural smartphone buyers.

Mobile Ki Dukaan Summary

India’s smartphone market in Q1 2026 tells a very clear story. Shipments fell, prices rose and entry-level phones took the biggest hit. But the market did not stop moving. Buyers shifted upward, offline retail became stronger and brands with better mid-range execution gained ground.

For Rajasthan buyers, the smart approach is to focus on value, not just lowest price. A phone with better RAM, storage, battery, service support and exchange value may be a better deal than the cheapest option available.

One important Rajasthan shop-level insight is that customers may delay buying because they expect prices to return to normal. At the same time, older near-EOL phones launched six months to one year ago may become more attractive if the gap versus new launch models widens from around ₹2,000 earlier to ₹4,000-₹6,000 now. This can help old stuck stock move out, but it can also slow fresh stock sales and new imports.

For mobile shops, this is a serious moment. Customers will need more explanation, more comparison and more trust. Shops that guide buyers properly, show clear pricing, offer exchange support and explain EMI carefully can benefit from the offline retail recovery.

The biggest question for the rest of 2026 is simple: will brands absorb the cost pressure or pass more of it to customers? If prices keep rising, India’s smartphone market may become more value-driven, more finance-led and more dependent on trusted local mobile shops.

.webp)